Choosing the legal structure for your startup company requires careful evaluation of a number of legal and business considerations. The following provides an overview of key aspects to consider during the business formation of your new company.

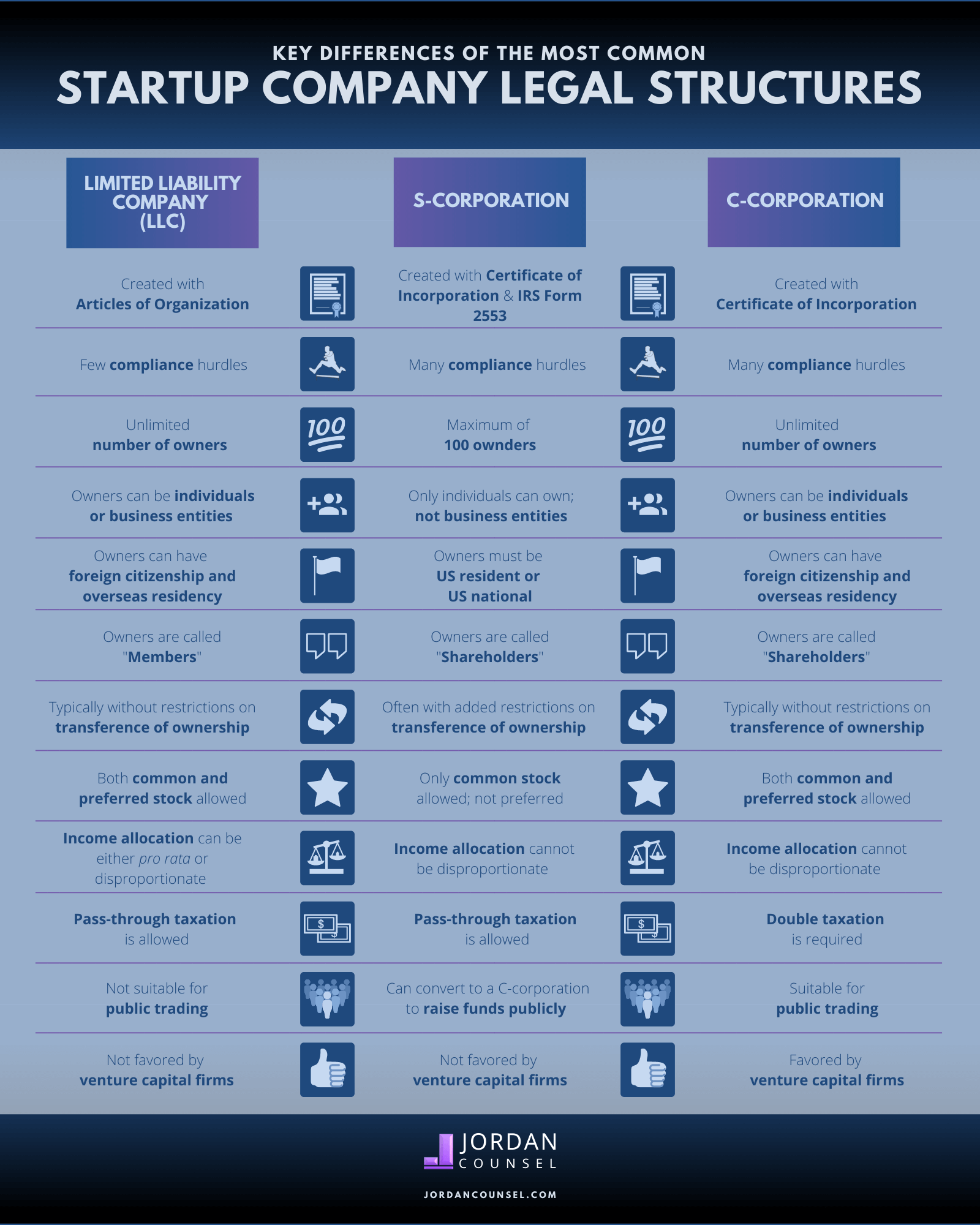

Ownership: First, some basics. Corporations are owned by shareholders, while LLCs are owned by members. S-corporations are peculiar in their ownership restrictions. Firstly, all S-corporation owners must be US nationals or US residents. Secondly, the maximum number of shareholders in an S-corporation is 100. In contrast, C-corporations and LLCs allow ownership by business entities and foreign owners.

Complexity: Both C-corporations and S-corporations are more complex than LLCs. Much more complex. The burden of setting up a corporation includes corporate governance activities like establishing a board of directors, filing annual reports, holding shareholder meetings and keeping minutes of meetings.

In contrast, the regulatory compliance hurdles of the LLC are much lower. The founding members of LLCs have much more discretion in how they wish to operate, as long as they comply with their respective operating agreements.

Source of capital: If you are currently seeking venture funding or are planning on taking your company public in the near future, the C-corporation will likely be your preferred structure. However, most start-up companies—even if their ultimate goal is to be publicly listed—are not yet at this juncture and would benefit instead from the more simple LLC structure.

But what if you prefer the simple LLC structure yet strongly suspect you will need to convert to a C-corporation structure at some point down the road (eg, in a few years) to raise capital? There is a solution: get creative in drafting your founding papers! For example, your lawyer can draft your LLC’s Operating Agreement to ‘mimic’ a corporate Shareholder’s Agreement. With that mimicking your lawyer could structure your equity in the form of “units of membership interests” (an absolute number, similar to shares), rather than an LLC’s typical “membership interest” (a percentage). As a result, a subsequent conversion to a C-corporation should be less complicated.

Allocation of ownership and income: LLCs and C-corporations can have common stock and preferred stock (eg, with premium returns and/or superior voting rights). By contrast, S-corporations do not allow differentiation of shares besides voting and non-voting.

In C-corporations and S-corporations, income is allocated based on pro rata ownership of shares. In contrast, an LLC’s income can be allocated among the owners either proportionally or disproportionally (if there is a rational business justification).

Income taxation: You probably know that corporations look for ways to lower their tax burden. This is because a C-corporation is deemed to be its own legal person or entity and as such carries its own tax liabilities and must file its own tax returns at the federal level (to the Internal Revenue Service) and, where appropriate, at the state level. If the C-corporation is profitable and distributes dividends to its individual shareholders, those shareholders must report that income (from the dividends) on their personal income tax returns. So in essence the C-corporation’s earnings are ultimately taxed twice; hence the term “double taxation”.

In contrast, in the context of federal income tax the LLC and the S-corporation can almost be considered ghosts, because their earnings are “passed through” and just reported on the personal income tax returns of the LLC’s members and the S-corporation’s shareholders. This pass-through tax treatment can be a significant benefit, as it may result in significant fiscal savings for the LLC members and S-corporation’s shareholders.

But is pass-through taxation the best option for your startup company? When making that decision, consider your company’s growth plans. When a C-corporation reinvests its profits directly back into the company rather than distributing dividends, the personal tax burden of its individual shareholders is reduced. When an LLC reinvests its profits directly back into the company, the individual owners still realize a tax liability.

In summary, your choice of entity for your startup company may result in numerous benefits and/or limitations. To fully understand these implications and to make the best decision for your startup, consider discussing your goals and business plan with an accountant or one of our lawyers.